Three Big Ideas #64

Defence dividends, misleading metrics, and Brussels sprouts a problem

🪖 Mann Virdee, Head of Science and Technology

Navigating the world of defence procurement is notoriously difficult as a small firm. The new Defence Investment Plan, published yesterday, seeks to change that. I’m sure many entrepreneurs will welcome this, while others will naturally be more sceptical and will want to see it to believe it.

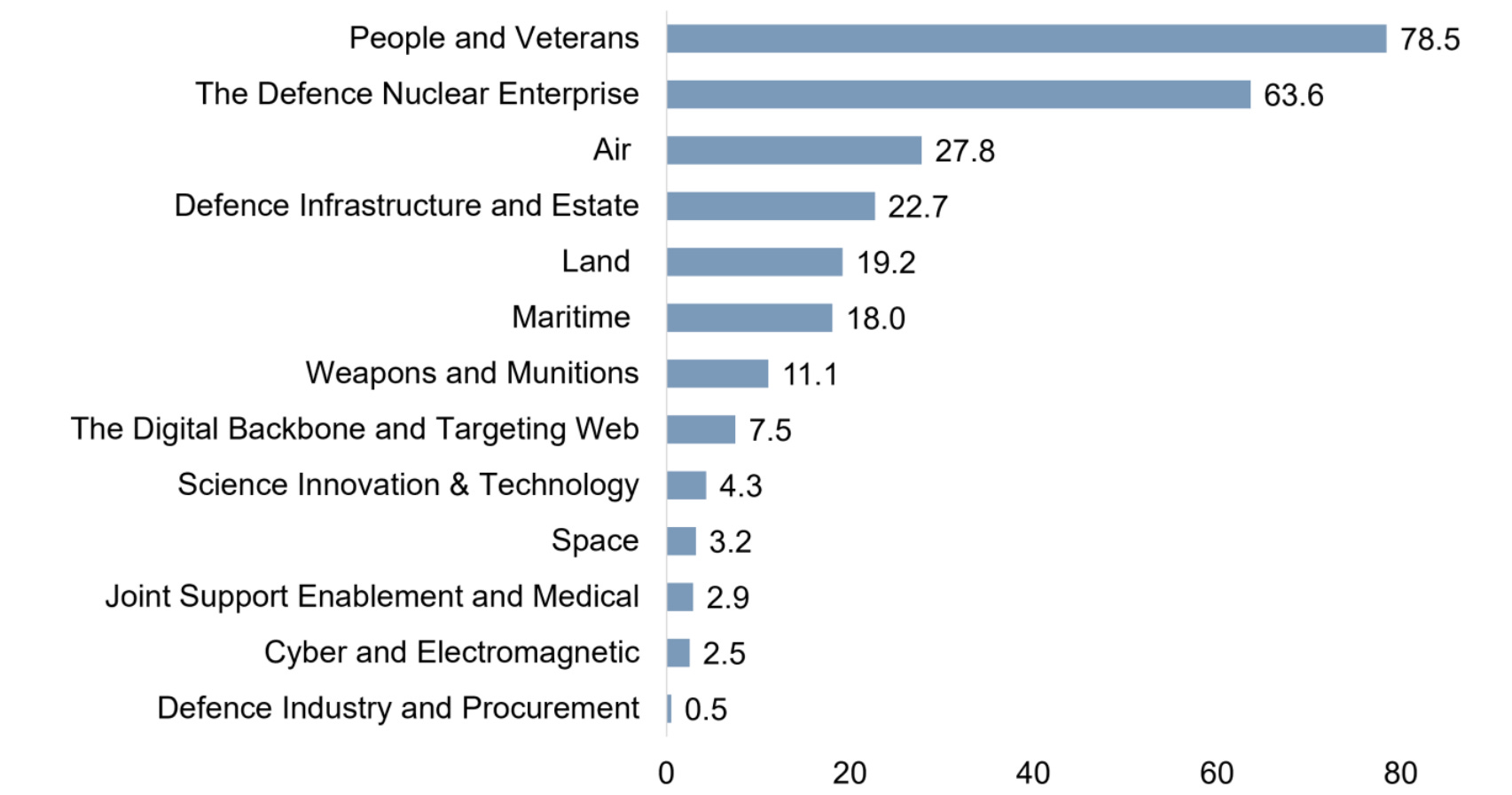

The headline figure is an increase in defence spending of £15 billion, funded from cuts to some road and energy projects – perhaps the last places such funding should come from.

The Plan explicitly frames defence as an engine for growth. Underneath some of the larger stories about submarines, sixth-generation fighters and drones, entrepreneurs will note that government is trying to become a better customer. There’s a commitment to spending an additional £2.5 billion through SMEs by 2028, representing a 50% increase in direct spend. That will be through the Defence Office for Small Business Growth, which was created at the start of this year.

Alongside this, there’s UK Defence Innovation, backed by £1.6 billion. That funding will be used to work with startups, scaleups and spin-outs to enable innovation in defence at ‘wartime pace’. The Plan also states that it aims to deliver ‘the next UK Defence unicorn’, with up to £100 million in accelerated contracts for British tech firms that have had limited or no current business with the Ministry of Defence (MoD).

This procurement-as-de-risking is one of the key ways the MoD can support entrepreneurs. When government sends clear demand signals and commits to buy, it helps SMEs cross the valley of death that kills so many promising firms between prototype and market. It’s the same logic that underpins Advance Market Commitments.

The last SME target, 25% of MoD spend, was technically met – but this was mostly through indirect spending via prime contractors. Direct spending with SMEs has remained around 4-5% (compared with 25% in the US), and as the government has noted, this figure has been falling. So this signal is welcome, but whether it will survive the transition to the next Government and actually deliver remains to be seen.

📈 Philip Salter, Founder

For decades, the official figures have shown the British economy is barely moving — a percent or two of growth in a good year. Yet, the ingenious entrepreneurs I meet week in week out, building incredible things at an astonishing rate, are suggestive of a more optimistic reality.

In When GDP Misleads: Inferring Living Standards from the Value of a Statistical Life, Stanford economists Philip Trammell and Charles I. Jones argue that GDP is poorly suited to counting the things that improve our lives most: namely, new goods, higher-quality goods, and the improvements that never register as a price at all. They open with Nathan Rothschild, the richest man in the world in the 1830s, who died at 58 in 1836 of an infection that $10 of antibiotics could likely cure today.

Picture an economy of two goods — food, which we get better at producing every year, and string quartets, which take the same four musicians they always have. As food gets cheaper, people spend a growing share of their money on music — and since the growth rate is a reflection of spending, the rate drifts downwards. Push that to its conclusion and you reach the absurd result that we would have been richer had the string quartet never been invented. A slowing growth rate, then, can be the mark of an economy rich enough to afford the finer things.

Progress comes from invention, not accumulation — and invention is precisely what GDP is worst at counting. The Trammell and Jones alternative is to use the value of a statistical life (VSL) — namely, what people will pay to reduce their risk of dying by a fraction. That figure reflects how much they value being alive, so it sweeps up everything that makes life better, new goods included. From this you can infer how fast living standards are really rising. As James Pethokoukis explains:

“The authors get at VSL partly by looking at the extra pay workers require to take more dangerous jobs. If workers need $1,000 more per year to accept a job with one extra death per 10,000 workers, that implies a statistical-life value of about $10 million.”

On the authors’ baseline, American lifetime wellbeing has risen five- to sevenfold since 1940. The usual consumption-based measures suggest it has merely doubled.

As the authors point out, the answer moves a great deal depending on the interest rate you assume. On less generous assumptions the gains shrink, or vanish. As Eamonn Ives has argued here, GDP shouldn’t be dismissed entirely. But we should be awake to the risk that relying on it too heavily understates both how much innovation is worth to us and the cost of putting up barriers to it.

🏛️ Ian Ng, Researcher

A report published by GovAI analysed 375 LLM releases over the past eight years and found that 11% were delayed or never released to the EU, with the figure standing at 7% for the UK. While the UK saw no delay in accessing the single most capable model at any point, it is still concerning when states are increasingly relying on frontier models for cyberdefence. Any delay in access, while hostile actors face no such constraint, could open a dangerous gap.

The authors attribute most delays and non-releases to regulatory factors, with data protection law the main barrier. Although the UK inherited most of its data regime from the EU, the authors point to the EU’s slower clarification of regulations and its more fragmented enforcement as the reason why barriers were higher across the Channel. They also note that the overall decline in delays may reflect labs building more mature compliance functions and greater regulatory certainty over time.

If Europe wants homegrown startups building frontier models, it needs to reduce the regulatory burden on them. The fewer resources a startup must dedicate to navigating regulatory uncertainty, the more it can spend on building. The regulations also risk becoming an entrance barrier for startups while protecting incumbents with large legal teams from competition.

We may also be witnessing the fading away of the Brussels Effect. The Brussels Effect held that EU regulations would set the global standard because it’s easier for businesses to comply with the strictest rule than to maintain a separate product. However, we are increasingly seeing the European market being carved out from the initial rollout of emerging tech products owing to regulatory uncertainty. As the authors have noted, Meta’s Threads and Apple Intelligence were both delayed in their European releases to comply with the Digital Markets Act.

When the term Brussels Effect was coined in 2012, the EU’s GDP was roughly a quarter of the world’s — today it stands at approximately one-sixth. Mounting regulatory uncertainty sits poorly with a shrinking market, and it is only making it more convenient for emerging tech companies to delay or completely avoid rolling out their products in Europe.

GovAI researchers found no evidence the EU AI Act itself has yet caused a single delay, but the enforcement of its general-purpose AI rules will only begin this August. The EU is about to run that experiment in real time. Britain’s advantage is that it doesn’t have to follow it down the same path.