Three Big Ideas #61

Metrics that matter, TRL traps and SMEs on the front line

🧑💼 Philip Salter, Founder

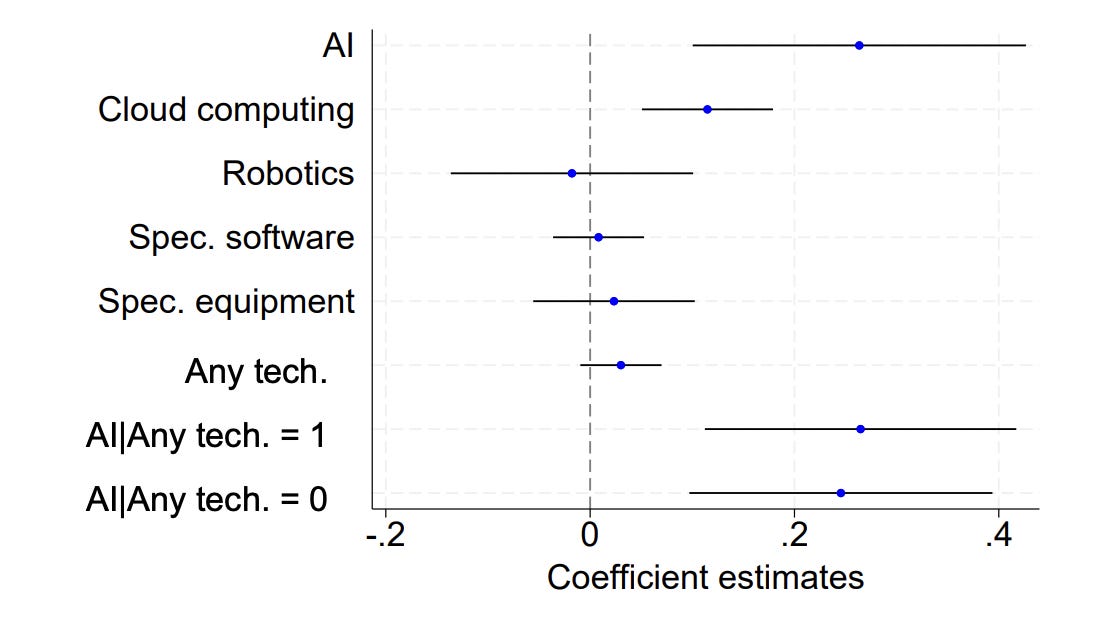

AI adoption is usually discussed in terms of cost and compute. In More Than Just Plug and Play, a working paper published this month, Diane Coyle and colleagues at the Bennett School use the ONS Management and Expectations Survey to show that UK firms with stronger management practices in 2020 were significantly more likely to go on to adopt AI by 2023.

Digging a bit deeper, it turns out different technologies call for different organisational capabilities. The same management practices that predict AI adoption show no relationship with the adoption of robotics, specialised software or specialised equipment.

We already know the UK has a management problem. Nick Bloom and John Van Reenen’s seminal 2007 paper introduced a structured way of measuring management practices across firms and countries, and the body of work that followed has consistently shown UK firms lagging US counterparts — with a particularly long tail of badly managed firms dragging down the productivity distribution. The policy response has tended to bundle this into general management improvement — training, peer learning and leadership development — rather than targeting the specific practices.

The new evidence narrows the target. As the paper notes, “it is specifically monitoring practices, such as use of KPIs and target-tracking, along with decentralised product development, that predict adoption.” Practices around continuous improvement and employment had weaker or insignificant effects.

Among multi-site firms, those where product development decisions sit closer to the frontline were more likely to adopt AI. The authors suggest “AI applications are more likely to be context-specific and require domain or technical knowledge to identify valuable use cases.” The combination of autonomy and measurement is the specific organisational structure that predicts AI adoption.

The policy implication is that management training interventions may be better targeted on capability-building around performance measurement and data architecture, combined with organisational design that empowers technical teams.

Policy aside, there’s a lesson here for founders bullish on AI. You don’t need a government programme to adopt the organisational shape this research describes. Building KPI infrastructure and pushing product decisions closer to the people who understand the work is something firms can do on their own. The companies that get this right won’t be waiting for policy to catch up. (Mann picks up the structural side of this problem below.)

💻 Mann Virdee, Head of Science and Technology

The OECD, in collaboration with the Department for Science, Innovation and Technology, recently released a report on technology adoption in the UK.

On the one hand, their findings indicate that British firms do well on mature digital technologies. The UK’s adoption of cloud computing, data analytics and basic process tools sits above EU and OECD averages, and SMEs have largely closed the gap with larger firms in using these foundational tools. On the other hand, for more advanced technologies, such as AI, robotics and automation, uptake is more limited than one would expect for a country with the UK’s income level (see Philip’s article above).

Take robotics, for example. The UK has a strong manufacturing legacy, particularly in the Midlands — yet adoption of robotics among manufacturing firms trails the EU average. The OECD attributes this to a mix of factors that compound in smaller manufacturers: high upfront costs, the average age of business owners, distrust of technology vendors, and a ‘wait-and-see’ approach whereby firms only adopt after peer validation. Each barrier is manageable in isolation, but together they create a structural drag on uptake in the sector in which the productivity dividend should be largest.

Geography compounds this problem. The OECD’s data on regional adoption finds that between 2018 and 2022, average SME adoption of AI and robotics technologies stood at around 15% in London and the South-East, but just 1.9% in the North-East. The concentration in the Golden Triangle is well-documented, but the within-region picture is just as stark. In the West Midlands, the Black Country trails most innovation indicators despite sitting next to one of the UK’s strongest industrial clusters.

The OECD’s overarching diagnosis is that Britain supports research well through to prototype (Technology Readiness Level (TRL) 6–7), but that support thins out at the stage of demonstration at scale, customer validation and early market entry (TRL 8–9). It’s at the later stage that firms package innovations into off-the-shelf products with the reliability and support that allow non-frontier SMEs to adopt them. Without that later stage of support, brilliant science struggles to become widely diffused technology.

The report’s proposed solution is to expand the commercialisation role of the Catapults, paired with the British Business Bank to crowd in private co-investment. For our part at The Entrepreneurs Network, we’ve been bringing together robotics founders with the Regulatory Innovation Office and the Health and Safety Executive to try to make their scaling journey smoother — exactly the kind of intermediary work the TRL 8–9 gap demands at scale.

🛡️ Harry Pitts, University of Exeter

Britain’s drive towards defence reindustrialisation and rearmament will depend on whether smaller, more agile firms can be integrated into the defence supply chain. In a new report for Babcock, The Next Line of Defence: Unlocking SME Potential in UK Defence from Policy to Practice, our team at the University of Exeter’s Defence, Security & Resilience Network found that the primary barriers relate to culture and process.

We interviewed 20 cutting-edge defence SMEs, both those well-established in the supply chain and those pivoting in from civilian sectors. The picture that emerged is of significant capability waiting to be unlocked, set against procurement systems that struggle to engage with it.

Ukraine’s high-tech resistance to Russia’s invasion has demonstrated what agile, software-led innovation can do on the modern battlefield. The UK has firms capable of producing similar capabilities at pace, but defence procurement, administrative systems and financing frameworks remain designed around large, established suppliers operating on multi-year cycles.

SMEs need credible demand signals to justify the investment and recruitment that scaling for defence requires. The forthcoming Defence Investment Plan is the obvious vehicle, and its credibility with the SME community will depend on how concretely it signals where money will flow and over what timeframe.

There is also a vital role for primes — the large, established contractors that sit between government and the SME base. Our interviews suggest that the most productive prime–SME relationships invert the usual power dynamic, with primes acting as supporting partners that help smaller companies articulate the value of their products to government, navigate procurement processes and bridge the gap between SME agility and government risk aversion. This is a markedly different role from the traditional one of subcontracting work down a tiered supply chain.

Babcock’s SME Engagement Charter, informed by our evidence, is an attempt to formalise this. Against a backdrop of rapid geopolitical change, primes have the power to realise in practice the promise of government policy in this domain.